Dear "Internal Revenue

Service",

In your letter in the Form 1040

Instruction booklet, it was stated: "Providing

information about our tax laws or your account status when you want it is

another of our priorities.” I trust,

therefore, that providing direct and specific answers to the enclosed questions

concerning the tax laws will be a high priority for your office.

Please note: I am not attempting, by writing this

letter, citing the findings contained herein, or by asking the questions

enclosed, to express or reflect personal opinion or frustration with the tax

system. Nor does this letter in any way reflect my advocating the violation of or

noncompliance with any internal revenue laws. I am not attempting, by writing

this letter, to enter into a debate regarding the legality of 26 USC, the tax

laws, the Constitution or any of its Amendments. I am not protesting any tax. I

am simply requesting information via this letter pursuant to the above

referenced Revenue Rulings, and pursuant to your stated priority to provide

information to me concerning the tax laws.

Please do not respond to me with a

letter stating that I have written some unspecified "type of letter"

reflecting personal opinions or frustration with the tax system, unless you

specifically cite which of my questions specifically reflects personal opinions

or frustrations with the tax system.

Please also do not state that

"it would be unfortunate if you were to rely on opinions of those who

deliberately promote violation of the laws passed by Congress," since I do

not rely on opinions, only on statutes, regulations and other government

documents, and I most certainly do not rely on, nor do I wish to rely on, the

opinions of anyone who deliberately promotes the violation of the laws passed

by Congress. This letter contains technical questions concerning statutes,

regulations and other government documents.

In addition, I am requesting that

you not respond to this request by merely citing 26 U.S.C.§

7802 and § 7803, as I deal with those sections in this letter, and why they do

not constitute a proper response to this "request for information.” I have been studying, reading and searching for

several years to find, within Title 26 of the United States Code, the Internal

Revenue Code, the section or sections which created your agency, the so called

"Internal Revenue Service"; but, I have been unable to find any

such specific statutes or sections. I decided to research and locate whatever

other sources of information I could find regarding how the entity which calls

itself "Internal Revenue Service" was established; what my research has uncovered is

strange and confusing. Here are some of the things, which I have found:

In 1972, an Internal Revenue Manual

("IRM") 1100 was published in both the Federal Register and the

Cumulative Bulletin; see 37 Fed Reg.

20960, 1972-2 Cum. Bul. 836. On the very first page

of this statement published in the Bulletin, the following admission was made.

(I have emphasized the significant sections):

"(3) By common parlance and

understanding of the time, an office of the importance of the Office of

Commissioner of Internal Revenue was a bureau. The Secretary of the Treasury in

his report at the close of the calendar year 1862 stated that ‘‘The Bureau of

Internal Revenue has been organized under the Act of the last session’’ Also it

can be seen that Congress had intended to establish a Bureau of Internal

Revenue, or thought they had, from the act of March 3, 1863, in which provision

was made for the President to appoint with Senate confirmation a Deputy

Commissioner of Internal Revenue ‘‘who shall be charged with such duties in the

bureau of internal revenue as may be prescribed by the Secretary of the

Treasury, or as may be required by law, and who shall act as Commissioner of

internal revenue in the absence of that officer, and exercise the privilege of

franking all letters and documents pertaining to the office of internal

revenue.’’ In other words, ‘‘the office of internal revenue’’ was ‘‘the bureau

of internal revenue,’’ and the act of July 1, 1862 is the organic act of

today’s Internal Revenue Service."

This

statement, which appears again in a similar publication appearing at 39 Fed. Reg. 11572,

1974-1 Cum. Bul. 440, as well as

the current IRM 1100, essentially admits that Congress never created either the

Bureau of Internal Revenue, or the Internal Revenue Service. To conclude that

"it can be seen that Congress had intended to establish a Bureau of

Internal Revenue, or thought they had" (see IRM 1111.2 -- Organic Act)

(Emphasis added) -- is an admission that even the government itself cannot find

anything whatsoever which actually created either agency. The only office created by the act of July 1,

1862, was the Office of the Commissioner of Internal Revenue (not the

Commissioner of Internal Revenue Service); neither the Bureau of Internal

Revenue, nor the "Internal Revenue Service" was created by any of

these acts.

I have no doubt that, when the

employees of the "Internal Revenue Service", and, perhaps others,

were researching the origins of the so-called agency so that this statement

could be included in the IRM 1100, these employees must have performed a very thorough

and exhaustive investigation. I am sure that the position of the "Internal

Revenue Service" regarding how the alleged "Internal Revenue

Service" came into being is the best that could be written under these

circumstances.

However, besides the problem that

these acts simply did not create either the "Bureau of Internal

Revenue" or the "Internal Revenue Service", there exists the

fact that these acts were repealed by the adoption of the Revised Statutes of

1873. Therefore, it would appear that your "agency" has never

actually been created by any act of Congress.

This is obviously a serious flaw,

and creates some valid and serious legal problems. Furthermore, I have

discovered the following: There was an

entity known as the "Bureau of Internal Revenue" which was renamed

"Internal Revenue Service", as revealed by Department of Treasury

Order 150-06, dated July 9, 1953 (see below) and further, by Treasury Decision

6038, entitled "Change of Nomenclature". However, an examination of

the General Records of the Department of the Treasury (Record Group 56)

1789-1990, 56.1, Administrative History, from the National Archives and Record

Administration reveals that no agency/entity called "Bureau of Internal

Revenue" is listed in the "Former administrative units of the

Treasury Department". In addition, the National Archives and Record

Administration states:

"The Tax Act of 1862 authorized

a permanent internal revenue establishment, the Office of the Commissioner of

Internal Revenue, which supervised a network of district collectors and

assessors and other field agents, and which was informally known as the Bureau

of Internal Revenue. It was formally re-designated the IRS, 1953." (Emphasis

added.) "Informally

known" means that no such agency was ever statutorily created, and that an

"informally known" nickname was renamed ("re- designated")

"IRS" in 1953. I have

also found the following statement in the Federal Register, Volume 41, September 15th, 1976:

"The term ‘‘Director, Alcohol, Tobacco and Firearms Division’’

has been replaced by the term ‘‘Internal Revenue Service.’’

What the above makes clear is that

"Internal Revenue Service" is, at least in this case, simply another

name -- an alias or as the Federal Register clearly states, a "term"

-- for the term "Director, Alcohol, Tobacco and Firearms Division",

which is itself (as stated) a term, and not an agency which Congress has ever

created.

I have also located the following

documents: 27 CFR § 201, which is

entitled "Short title", is cited as the

"Federal Alcohol Administration Act.”

In § 201, under HISTORY:

ANCILLARY LAWS AND DIRECTIVES is found the following: "Transfer of functions: Federal Alcohol Administration and offices of

members and Administrator thereof were abolished and their functions directed

to be administered under direction and supervision of Secretary of Treasury

through Bureau of Internal Revenue [now Internal Revenue Service] in Department

of Treasury, by Reorg. Plan No. 3 of 1940 which

appears as 5 USCS § 903 note The Department of the Treasury Order 221 of July

1, 1972, established the Bureau of Alcohol, Tobacco and Firearms and

transferred to it the alcohol and functions of the Internal Revenue

Service.” (Emphasis added.)

The last sentence is correctly

quoted: "the alcohol and

functions". This last sentence of the above section clearly states

that "the functions" of the Internal Revenue Service were

"transferred" to the Bureau of Alcohol, Tobacco and Firearms when the

BATF was established. The term used in this cite is "the functions",

not "some of the functions", or "certain functions", or any

other term, which would imply a limited transfer of specific, limited

functions. The use of the all-inclusive term, "the functions, "thus

implies that all functions of "IRS" were transferred to BATF upon BATF’s establishment. If all of "the functions"

of "IRS" were transferred to BATF upon BATF’s

establishment, then which specific "functions" does "IRS"

handle at present, if any?

I have located the actual document

which established the Bureau of Alcohol, Tobacco and Firearms, Treasury Order

120-01, (a renumbering of DOT Order 221) which is entitled "Establishment

of the Bureau of Alcohol, Tobacco and Firearms". TO 120-01 cites various

functions and provisions of law, which have been delegated to the BATF.

In paragraph #2, section b, TO

120-01 states that Chapters 61 through 80, inclusive, of the Internal Revenue

Code are delegated to BATF "insofar as they relate to the activities

administered and enforced with respect to Chapters 51, 52 and 53;"

Chapters 61 through 80, also known as Subtitle F of the Code, contain all of

the "Procedures and Administration" statutes for filing returns,

assessment, collection, interest, penalties, crimes, other offenses and

forfeitures, and liability and enforcement of tax. Some of the sections found

in Chapters 61 through 80 of Title 26, the Internal Revenue Code, sections that

many people would recognize, are the following:

§ 6001 ("Notice or regulations

requiring records, statements and special returns")

§ 6011 ("General requirement of

return, statement or list")

§ 6012 ("Persons required to

make returns of income" a, b and c are all cited in the "IRS"

Form 1040 Instruction booklet as the government’s authority to ask for

information.)

§ 6321 ("Lien for taxes")

§ 6331 ("Levy and distraint")

§ 7201 ("Attempt to evade or

defeat tax")

§ 7203 ("Willful failure to

file return, supply information, or pay tax")

§ 7321 ("Authority to seize

property subject to forfeiture") (For more on this section, and how it

appears only relevant to BATF, see below.)

It is true that Chapters 51, 52 and

53 are entitled respectively "Distilled Spirits, Wines, and Beer",

"Cigars, Cigarettes, Smokeless Tobacco, Pipe Tobacco, and Cigarette Papers

and Tubes", and "Machine Guns, Destructive Devices, and Certain Other

Firearms" – i.e., Alcohol,

Tobacco and Firearms -- which would seem to limit the authority of BATF

relevant to Subtitle F to alcohol, tobacco and firearms related

"Procedures and Administration". However, I cannot find anywhere a

statute or regulation or any other document, which delegates Chapters 61

through 80 of the Code to "Internal Revenue Service". And since

"the functions" of "IRS" were transferred to BATF by DOT

Order 221 upon BATF’s creation in 1972, then it seems

clear that all of the above-cited Procedures and Administration

"functions" are under the jurisdiction of BATF alone.

What seems to me to be true is that

all crimes which are committed relevant to Chapters 61 through 80 of the Code appear to actually be a violation of BATF laws, and not

"IRS" laws. In addition, 27 CFR §§ 70.11 also states that Subtitle F

is delegated to be enforced and administered by BATF, "as it relates to

any of the foregoing."

The words "the foregoing" in

27 CFR §§ 70.11, which is a section entitled "Meaning of terms",

refer to the following terms:

Person; lien; levy;

enforced collection; electronic

fund transfer; Director (BATF); Commercial Bank; Chief, Tax Processing Center; Code of Federal Regulations; Bureau;

ATF Officer. So 27 CFR §§ 70.11 is stating that BATF has been delegated

the authority of Subtitle F as it relates to liens, levies, enforced collection

(i.e., seizure and forfeiture) --

activities which one generally associates with "IRS". Again, I can

find no such delegation of authority to "IRS" which relates to such

activities. This regulation further appears to make it clear that it is really

BATF, which is liening, levying and seizing property,

even when it appears that "IRS" is doing these things.

This is a significant

conclusion: it appears that it is always

BATF, which is masquerading as "IRS" when "IRS" is liening, levying and seizing property. This conclusion is

further supported by 26 USC §§ 7321, which is the section of the Internal

Revenue Code entitled "Authority to Seize Property Subject to

Forfeiture". It states: "Any property subject to forfeiture

to the United States under any provision of this title may be seized by the

Secretary."

Then, in the implementing regulation,

26 CFR §§ 301.7321 -- 1, entitled "Seizure of Property", is stated

the following:

"Any property subject to

forfeiture to the United States under any provision of the Code may be seized

by the district director or assistant regional commissioner (alcohol, tobacco

and firearms). Upon seizure of property by the district director he shall

notify the assistant regional commissioner (alcohol, tobacco and firearms) for

the region wherein the district is located who will take charge of the property

and arrange for its disposal or retention under the provisions of law and

regulations applicable thereto.”

(Emphasis added.)

The above statute and regulation

plainly reveal that all property which is seized by IRS under any provision of

Title 26, whether it be by the district director or the assistant regional

commissioner (alcohol, tobacco and firearms), is then handed over to the

assistant regional commissioner (alcohol, tobacco and firearms), who

"arrange(s) for its disposal and retention." Why is all property seized by "IRS"

-- "under any provision of Title 26" (which would, of course, include

Subtitle A, "Income Taxes" -- much of it having to do with alleged

violations of "income tax" laws, and ostensibly having nothing whatsoever

to do with alcohol, tobacco or firearms taxes) seized by the district director,

and then handed over to this mysterious assistant regional commissioner

(alcohol, tobacco and firearms), who clearly appears to be either an official

of the Bureau of Alcohol, Tobacco and Firearms, or perhaps an official relevant

only to Chapters 51, 52 and 53 of the Internal Revenue Code?

It could only be because somehow all

of the laws in Chapters 61 through 80, including the seizure and forfeiture

laws of the IRC, are relevant only to BATF taxes. Also in TO 120-01 (dated

6/6/72) is a reference to the term "Director, Alcohol, Tobacco and

Firearms Division" -- the same term which was renamed "Internal

Revenue Service" according to the Federal Register of 9/15/76 (see above.)

TO 120-01 states:

"The terms ‘‘Director, Alcohol,

Tobacco and Firearms Division’’ and ‘‘Commissioner of Internal Revenue’’

wherever used in regulations, rules, and instructions, and forms, issued or

adopted for the administration and enforcement of the laws specified in

paragraph 2 hereof, which are in effect or in use on the effective date of this

Order, shall be held to mean the Director"

"The terms ‘‘internal revenue

officer’’ and ‘‘officer, employee or agent of the internal revenue’’ wherever used

in such regulations, rules, instructions and forms, in any law specified in

paragraph 2 above, and in 18 U.S.C. 1114, shall include all officers and

employees of the United States engaged in the administration and enforcement of

the laws administered by the Bureau, who are appointed or employed by, or

pursuant to the authority of, or who are subject to the directions,

instructions or orders of, the Secretary."

The above statements -- aside from

being extremely circular and difficult to follow -- appear to be revealing that

the official known as the Commissioner of Internal Revenue is actually the same

person and office as the Director, Alcohol, Tobacco and Firearms Division (who

was renamed "Internal Revenue Service" according to the Federal

Register, Volume 41, Wednesday, September 15, 1976) and that the officials

known as "internal revenue officer" and "officer, employee or

agent of the internal revenue" are actually enforcing BATF laws. For

further exploration of this, see the definition of "Revenue Agent"

below.

TO 120-01 goes on to state: "There shall be transferred to the

Bureau all positions, personnel, records, property, and unexpended balances of

appropriations, allocations, and other funds of the Alcohol, Tobacco and

Firearms Division of the Internal Revenue Service, including those of the

Assistant Regional Commissioners (Alcohol, Tobacco and Firearms), Internal

Revenue Service."

Commissioner Of Internal Revenue

Service -- the Assistant Regional Commissioner (Alcohol, Tobacco and Firearms)

is apparently the same official named in 26 CFR §§ 301.7321- 1, who "takes

charge" of all property seized by "IRS" and "arranges for

its disposal.” What is even more bizarre

is this: after all the property seized

by "IRS" is handed over by the district director to this mysterious

assistant regional commissioner (alcohol, tobacco and firearms), the remission

or mitigation of forfeitures relevant to the Internal Revenue Code (Title 26)

and its regulations (26 CFR) is governed by the customs laws which are applicable

to remission or mitigation of penalties as contained in Title 19 USC -- Customs

-- Sections 1613 and 1618. Sections 1613 and 1618 of Title 19 fall under

Chapter 4, which is relevant to the enforcement of the provisions of the Tariff

Act of 1930. Why are sections of the customs laws, which govern the enforcement

of the Tariff Act of 1930, the only laws which are cited to be used to remit or

mitigate forfeitures of property, which has been seized by "IRS" and

then handed over to a BATF official? More

simply: If my property were seized by

"IRS", why would I be forced to use Customs laws to attempt to get it

back?

Returning to the above cite from 27

CFR §§ 201, concerning the Federal Alcohol Administration, it is obvious that

some entity with the present name "Internal Revenue Service" used to

be known as the "Bureau of Internal Revenue.” And I find that renaming confirmed in

Treasury Order 150-06, dated July 9, 1953, entitled "Designation as

Internal Revenue Service," which states in paragraph #1: "The Bureau of Internal Revenue shall

hereafter be known as the Internal Revenue Service."

So, where did this "Bureau of

Internal Revenue" which was then renamed "Internal Revenue

Service" originate? The only

place I can find any reference whatsoever to the creation of a "Bureau of

Internal Revenue" is in Article I of the Philippine Commission Act, Act

No. 1189, dated 1904, which states in Section 2:

"There shall be established a

Bureau of Internal Revenue, the chief officer of which shall be known as the

Collector of Internal Revenue. He shall

be appointed by the Civil Governor, with advice and consent of the Philippine

Commission, and shall receive a salary at the rate of eight thousand pesos per

annum. "The Bureau of Internal Revenue shall belong to the Department of

Finance and Justice."

Does this mean that the Bureau of

Internal Revenue established in the Philippines in 1904 is the same Bureau of

Internal Revenue, which was renamed "Internal Revenue Service" in

Treasury Order 150-06? And, if not, what

is the statutory origin of the Bureau of Internal Revenue, which is cited in TO

150-06? And since the Bureau of Internal

Revenue established in the Philippines in 1904 belonged at that time to the

Department of Finance and Justice, if it is the Bureau of Internal Revenue,

which was renamed "Internal Revenue Service" and is now found in the

Department of the Treasury, how was it transferred from the former department

to the latter, and when?

In addition, I have looked in 31 U.S.C.,

Chapter 3, at the list of organizations of the Department of the Treasury; only to find that there is no "Internal

Revenue Service" listed there as an organization of the Department of the

Treasury. Further, research reveals that there is no "Internal Revenue

Service" listed as an agency, or even a term, within any of the

organizations listed in Chapter 3.

Also, in 31 U.S.C., in Section 1321,

the list of Trust Funds maintained by the Treasury, I have found the

following: Section 1321(2) and 1321(62)

are named respectively as follows:

"(2)

Philippine special fund (internal revenue).

(62) Puerto

Rico special fund (Internal Revenue)."

Again, I find a reference to the

Philippines (and Puerto Rico -- see below, 27 CFR § 250.11), with the words

"internal revenue" (and "Internal Revenue") used to define

the Philippines and Puerto Rico respectively. And the spelling and capitalization of the two

terms is the only thing which indicates which is the Philippine and which the

Puerto Rico special fund.

In reference to Puerto Rico, and

further questions concerning this issue, I have found in 27 CFR § 250.11 that

the definition of "Revenue Agent" is given as:

"Any duly authorized

Commonwealth Internal Revenue Agent of the Department of the Treasury of Puerto

Rico."

There, the definition of

"Secretary" is given as: "The

Secretary of the Department of the Treasury of Puerto Rico.” And there, the definition of

"Secretary or his delegate" is given as: "The Secretary or any officer or

employee of the Department of the Treasury of Puerto Rico duly authorized by

the Secretary to perform the function mentioned or described in this

part."

So, there apparently exists another

"Department of the Treasury" -- in Puerto Rico. Its official name is "The Department of

the Treasury of Puerto Rico", and it has a Secretary, delegates of its

Secretary, and Revenue Agents.

Does this mean that the

"Internal Revenue Service" is found somewhere in the Department of

the Treasury of Puerto Rico, since it isn’t found in the list of organizations

in the Department of the Treasury in Title 31, United States Code, or within

any of those listed organizations? Not

only that, but since the only definition of "Revenue Agent" which I

can find is that found in 27 CFR § 250.11, does this mean that all

"IRS" Revenue Agents actually work for the Department of the Treasury

of Puerto Rico?

I have found other statutes and

regulations, which are confusing to me:

at 48 USC § 1402 I find the following:

Title III of the National

Prohibition Act, as amended and all provisions of the internal revenue laws

relating to the enforcement thereof, are hereby extended to and made applicable

to [Puerto Rico and] the Virgin Islands"

I find still further, in the same

section, under HISTORY;

ANCILLARY LAWS AND DIRECTIVES:

"Title III of the National Prohibition Act", referred to in

this section, is Act Oct. 28, 1919, ch 85, Title III,

41 Stat. 319, which was generally classified to 27 USC § 71 et seq. prior to supersedure by the Internal Revenue Code of 1939, and

subsequently by the Internal Revenue Code of 1954."

The previous statement says to me

that Title III of the National Prohibition Act was classified through several

stages to the Internal Revenue Code (Title 26 of the United States Codes). That

conclusion is supported and confirmed by the following, found in the same

section: "The internal revenue

laws", referred to in this section, are located generally at 26 USCS § 1

et seq."

The Lawyers' Cooperative Publishing version (1995)

words the preceding section slightly differently:

"The internal revenue

laws", referred to in this section, appear generally as 26 USCS § 1 et

seq.” (Emphasis added.)

Commissioner of Internal Revenue

Service, as you know, 26 USCS is the Internal Revenue Code, and "§ 1 et seq.” means: "Section 1 and all which follows

it" -- i.e., the entire Code

from start to finish.

In other words, this cite from Title

48 (§ 1402) plainly states that the entire Internal Revenue Code, from start to

finish, is "generally" made up of "internal revenue laws"

which are relevant to the enforcement of Title III of the National Prohibition

Act, which is presently located in Puerto Rico and the Virgin Islands. In fact,

the Lawyers’’ Cooperative Publishing version of 48 USC § 1402 literally says

that 26 USCS -- the entire Code -- is only the "internal revenue

laws" relevant to the enforcement of Title III of the National Prohibition

Act, since it makes the statement: "The

"internal revenue laws" referred to in this section appear generally

as 26 USCS § 1 et seq."

This is truly strange. Obviously,

when I read the above statute, I must ask this question: Which internal revenue laws

"generally located at (or "which appear generally as") 26 USCS §

1 et seq.” -- the Internal Revenue

Code -- are relevant to anything other than or in addition to the enforcement

of Title III of the National Prohibition Act?

In addition, Internal Revenue Manual

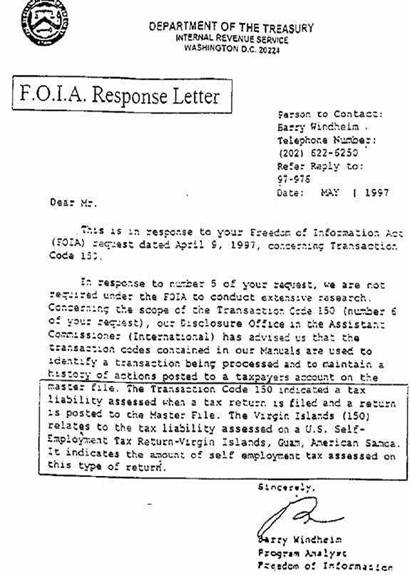

(IRM) 30(55)4.2 at (29) -- dated 1-1-90 -- reveals the following: "VIRGIN IS (TC 150)".

"TC" stands for

"Transaction Code", and "VIRGIN IS" stands for "Virgin

Islands.” As you know, a Transaction

Code (TC) 150 transcript (Individual Master File,

abbreviated IMF) is the computer transcript to which data is input either when

someone files a Form 1040, or a Substitute For Return (SFR) is filed by

"IRS.” Thus Form 1040 data is input

on a Virgin Is lands transcript, indicating a liability, payment, or other

action relevant to a Virgin Islands liability. 48 U.S.C. § 1402 states that

Title III of the National Prohibition Act, and all provisions of the internal

revenue laws relating to the enforcement thereof, have been extended to and

made applicable to [Puerto Rico and] the Virgin Islands.

The same section then goes on, as

you recall, to state that Title III of the National Prohibition Act was

reclassified to 27 U.S.C. § 71 et seq.,

and then to the Internal Revenue Code of 1939, and subsequently the Internal

Revenue Code of 1954. The section further states that the "internal

revenue laws" relevant to the enforcement of Title III of the National

Prohibition Act "are located generally at 26 USCS § 1 et seq."

What I surmise from the above is

that Title III of the National Prohibition Act was moved to [Puerto Rico and]

the Virgin Islands, and that the "internal revenue laws" relevant to

its enforcement are "located generally" throughout the Internal

Revenue Code, which means that they are internal revenue laws relevant, it

appears, to Puerto Rico and the Virgin Islands. I believe this is why the TC 150, which

indicates a Virgin Islands transcript, is posted to the IMF whenever a Form

1040 or SFR is filed. I believe this

indicates that the Form 1040 is actually a Virgin Islands return, and that I

would be committing perjury if I were to file Form 1040, since I am not liable

for filing a Virgin Islands return.

In fact, in Mills

v. United States, CIV-94-114-TUC- JMR, Fred D. Mills had caused to be filed

a Freedom of Information Act (FOIA) request to the Cheyenne District Office of

Internal Revenue Service requesting a copy of all documents maintained that

indicated that "TC 150 means other than and/or in addition to the Virgin

Islands.” The Internal Revenue Service

could produce no documents, which demonstrated that TC 150 is connected in the

geographical sense to other than the Virgin Islands. IRM 30(55) (4.2) at (29), [now 30(55)(4.2) at (30)] (which states, "VIRGIN IS (TC

150)"), was held by the Internal Revenue Service to be the only document

relevant to venue for TC 150. Loretta C.

Argrett, Assistant Attorney General, Tax Division,

stated in a letter dated January 9, 1995:

"no responsive documents exist" which would provide otherwise.

In fact, in Mills

v. United States, CIV-94-114-TUC- JMR, Fred D. Mills had caused to be filed

a Freedom of Information Act (FOIA) request to the Cheyenne District Office of

Internal Revenue Service requesting a copy of all documents maintained that

indicated that "TC 150 means other than and/or in addition to the Virgin

Islands.” The Internal Revenue Service

could produce no documents, which demonstrated that TC 150 is connected in the

geographical sense to other than the Virgin Islands. IRM 30(55) (4.2) at (29), [now 30(55)(4.2) at (30)] (which states, "VIRGIN IS (TC

150)"), was held by the Internal Revenue Service to be the only document

relevant to venue for TC 150. Loretta C.

Argrett, Assistant Attorney General, Tax Division,

stated in a letter dated January 9, 1995:

"no responsive documents exist" which would provide otherwise.

Perhaps this connection between the

Virgin Islands and Title III of the National Prohibition Act is why the

assistant regional commissioner (alcohol, tobacco and firearms) ends up with

all the property seized by "IRS" under any provision of Title 26 --

which itself appears to be the collection of "internal revenue laws"

relevant to the enforcement of Title III of the National Prohibition Act, an

Act which it seems to us that the Bureau of Alcohol, Tobacco and Firearms, not

"IRS", would be responsible for enforcing.

In addition, I have uncovered the

following: Form 1040 is entitled

"U.S. Individual Income Tax Return", which would indicate that it is

a form to be filed by a "U.S. Individual.”

26 CFR §§ 1.6017-1(a)(1), dealing with "Self-Employment tax

returns", states the following:

"an individual who is a resident of the Virgin Islands, Puerto

Rico, or (for any taxable year beginning after 1960) Guam or American Samoa is

not to be considered a nonresident alien individual.” 26 CFR § 1.6017-1(a)(2)

states: "Except as otherwise

provided in this subparagraph, the return required by this section shall be made

on Form 1040. The form to be used by residents of the Virgin Islands, Guam, or

American Samoa is Form 1040SS"

Internal Revenue Publication 676

states that Form 1040 SS is a "Self-Employment Tax Return.” But the above section states that the return

required "under this section shall be made on Form 1040.” It would appear, therefore, that an

"individual" is actually a resident of the Virgin Islands (or Puerto

Rico, or, before 1960, Guam or American Samoa). Perhaps that is why the TC 150, indicating

that a Virgin Islands return has been filed, is posted to the Virgin Islands

transcript IMF when a Form 1040 or SFR are filed. These facts have also been confirmed from the

above posted Freedom of Information Act Response as well.

So far, my research has brought me

to the following conclusions:

1. The only "Internal Revenue Service"

I can find is not an agency at all, but simply an alias (term replacement) for

the term "Director, Alcohol, Tobacco and Firearms Division," or else

the renaming of an entity called "Bureau of Internal Revenue", which

appears to have its origins in the Philippines in 1904.

2. There was never any "Bureau of

Internal Revenue" statutorily created by Congress. The term "Bureau

of Internal Revenue" was an "informal" nickname, not the name of

a statutory agency or entity. Therefore, the renaming of "Bureau of

Internal Revenue" as "Internal Revenue Service" is essentially

the renaming of a non- statutory nickname.

3. "Internal Revenue Service"

is not listed as an organization of the Department of the Treasury in Title 31,

but that there does exist in statute another "Department of the

Treasury" -- the Department of the Treasury of Puerto Rico -- which has a

"Secretary", and the Secretary’s "delegate(s)" and

"Revenue Agent (s)", and perhaps an "Internal Revenue

Service" although I have yet to locate such "agency" or

"term" therein.

4. "Internal Revenue" refers to the

Puerto Rico special fund, and "internal revenue" refers to the

Philippine special fund. Both of these appear to be trust funds maintained by

the Department of the Treasury of the United States -- not the Department of

the Treasury of Puerto Rico -- and it is only their respective spellings, which

make them completely different from each other.

5. The internal revenue laws relevant

to the enforcement of Title III of the National Prohibition Act are

"generally located at 26 USCS § 1 et

seq.” or "appear generally as

26 USCS § 1 et seq.", in other

words, throughout (or as) the entire Internal Revenue Code, and I have no way

of knowing which internal revenue laws in the Code are relevant to anything

other than and/or in addition to Title III of the National Prohibition Act.

Just the fact that many, or perhaps all, of the "internal revenue

laws" in Title 26 are clearly laws relevant to the enforcing of Title III

of the National Prohibition Act makes me wonder what relevance the internal

revenue laws contained in the Internal Revenue Code have to do with me. And how

am I to tell which of those laws are relevant to me -- if any?

6. All of the laws contained in Title 26, the

Internal Revenue Code, Chapters 61 through 80, are relevant only to BATF, and

not "IRS".

7. All property seized by IRS "under any

provision of the Code" (Title 26) is then handed over to an official whose

job title clearly defines him as dealing with alcohol and tobacco taxes. Why is property allegedly related to "income tax"

violations first seized by "IRS", and then handed over to the

assistant regional commissioner (alcohol, tobacco and firearms)?

8. The laws governing the remission and

mitigation of all of the property seized and forfeited under the provisions of

Title 26 are customs laws relevant to the enforcement of the provisions of the

Tariff Act of 1930. Why does one have to use customs laws to get back property

seized by "IRS"?

9. When one files a Form 1040, a Transaction Code

150, indicating a Virgin Islands return, is posted to the IMF, which IRS has

confirmed is a TC 150 transcript, and which the IRM indicates is a Virgin

Islands transcript.

Relevant to the creation of and

existence of an agency or office, at the state level, it is a well acknowledged

and accepted rule that a duly constituted office of the state government must

be created either by the state constitution itself, or else by some specific

legislative act; see the following: (All emphasis added). Patton v. Bd. of

Health, 127 Cal. 388, 393, 59 P. 702, 704 (1899) -- "One of the

requisites is that the office must be created by the constitution of the state

or it must be authorized by some statute."

First Nat. Bank of Columbus v.

State, 80 Neb. 597, 114 N.W. 772, 773 (1908); State ex rel.

Peyton v. Cunningham, 39 Mont. 197, 103 P. 497, 498 (1909); State ex

rel. Stage v. Mackie, 82 Conn. 398, 74 A. 759,

761 (1909); State ex rel. Key v. Bond, 94 W.Va. 255, 118

S.E. 276, 279 (1923) -- "a position is a public office when it is

created by law";

Coyne v. State, 22 Ohio App. 462,

153 N.E. 876, 877 (1926) -- "Unless the office existed there could be

no officer either de facto or de jure. A de facto officer is one invested with

an office; but

if there is no office with which to invest one, there can be no officer. An

office may exist only by duly constituted law".

This same rule applies at the

federal level; see United States v.

Germaine, 99 U.S. 508 (1879); Norton v.

Shelby County, 118 U.S. 425, 441, 6 S.Ct. 1121 (1886)

-- "there can be no officer, either de jure or de facto, if there be no

office to fill"; United States

v. Mouat, 124 U.S. 303, 8 S.Ct.

505 (1888); United States v. Smith, 124

U.S. 525, 8 S.Ct. 595 (1888); Glavey v. United

States, 182 U.S. 595, 607, 21 S.Ct. 891 (1901) -- "The

law creates the office, prescribes its duties"; Cochnower v.

United States, 248 U.S. 405, 407, 39 S.Ct. 137 (1919)

– "Primarily we may say that the creation of offices and the assignment

of their compensation is a legislative function.- And we think the delegation

of such function and the extent of its delegation must have clear _expression

or implication"; Burnap v. United States, 252 U.S. 512, 516, 40 S.Ct. 374, 376 (1920);

Metcalf & Eddy v. Mitchell, 269 U.S. 514, 46 S.Ct.

172, 173 (1926); N.L.R.B. v. Coca-Cola

Bottling Co. of Louisville, 350 U.S. 264, 269, 76 S.Ct.

383 (1956) -- "’’Officers’’ normally means those who hold defined offices.

It does not mean the boys in the back room or other agencies of invisible

government, whether in politics or in the trade-union movement"; Crowley v. Southern Ry.

Co., 139 F. 851, 853 (5th Cir. 1905);

Adams v. Murphy, 165 F. 304 (8th Cir. 1908); Sully v. United States, 193 F. 185, 187 (D.Nev. 1910) -- "There can be no offices of the

United States, strictly speaking, except those which are created by the

Constitution itself, or by an act of Congress"; Commissioner v. Harlan, 80 F.2d 660, 662

(9th Cir. 1935); Varden

v. Ridings, 20 F.Supp. 495 (E.D.Ky.

1937); Annoni v. Blas Nadal’’s

Heirs, 94 F.2d 513, 515 (1st Cir. 1938);

and Pope v. Commissioner, 138 F.2d 1006, 1009 (6th Cir. 1943).

In addition to the above-cited

cases, I am including selected paragraphs from a letter authored by Congressman

Pat Danner, 6th District, Missouri, to Bill Petterson,

Route 2, Box 37, Trenton, Missouri, 64683-9610. It is apparent from Congressman Danner’s

letter that Mr. Petterson has contacted him about

this question of the establishment of an agency known as "Internal Revenue

Service". The selected paragraphs

from Congressman Danner letter is enclosed herein and states, in unnumbered

paragraph #2:

"You are quite correct when

you state that an organization with the actual name "Internal Revenue

Service" was not established by law."

That statement appears to me to be

fairly clear and conclusive. Congressman

Danner then goes on, in the same paragraph, to state:

Instead, in 1862, Congress approved 26

U.S.C. 7802. This statute established the office of ‘‘Commissioner of Internal

Revenue.’’ As the act states, ‘‘The

Commissioner of Internal Revenue shall have such duties and powers as may be

prescribed by the Secretary of the Treasury.’’ In modern times, these duties and powers flow

to the Commissioner who implements appropriate policy through the IRS. "In addition to Section 7802, Section

7803 authorizes the Secretary of Treasury to employ such number of persons

deemed proper for the administration and enforcement of the internal revenue

laws. It is these employees who comprise

the IRS.” There are

several problems with Congressman Danner’s previous statement. These are as follows: Congress did not "approve" 26 USC

§§ 7802 in 1862. In reference to this

question, it has been stated: "[The

Act of June 30, 1926, 44 Stat. 777, Ch. 712], which created the 50 titles of

the United States Code is still in effect and is the foundation for the current

design of the United States Code. The

act did not repeal any prior laws or attempt to replace them. The titles and code sections contained therein

were only made prima facie evidence

of the laws of the United States. Their

use was suitable in court, but they could be impeached by showing what the

underlying statutes were and that the code sections were different from the

statutes; in

such event, the statutes controlled.

This condition prevails today for

those titles which are not positive law, and the same titles, or any particular

section thereof, can be impeached by showing a difference between the title or

code section and the underlying or supporting statutes; see Preston v. Heckler, 734 F.2d 1359,

1367 (9th Cir. 1983); and Rasquin v. Muccini, 72 F.2d 688

(2nd Cir. 1934)."

The "approval" to which

Congressman Danner is referring is the 1862 Act referenced in IRM 1111.2 in

which Congress "thought it had" established a Bureau of Internal

Revenue, and which clearly states that: "by

common parlance and understanding of the time, an office of the importance of

the Office of Commissioner of Internal Revenue was a bureau", and further,

"that Congress had intended to establish a Bureau of Internal Revenue, or

thought they had, from the act of March 3, 1862" (Emphasis added).

The "approval" to which Congressman

Danner is referring is the 1862 Act referenced in IRM 1111.2 in which Congress

"thought it had" established a Bureau of Internal Revenue, and which

clearly states that: "by common

parlance and understanding of the time, an office of the importance of the

Office of Commissioner of Internal Revenue was a bureau", and further,

"that Congress had intended to establish a Bureau of Internal Revenue, or

thought they had, from the act of March 3, 1862" (Emphasis added).

However, neither informal organic

growth, nor an "Organic Act" is enough to establish the statutory

foundation of a federal government agency. IRM 1111.2 does not, however, state

either that 26 U.S.C.§ 7802 was approved by Congress

in 1862, or that there was an official establishment of either a bureau or an

agency. And again, the only Bureau of

Internal Revenue, which I can find that was

established by Congress is the Philippine Bureau of Internal Revenue, described

above. And the National Archives lists

no "Bureau of Internal Revenue" in its list of "Former

administrative units of the Treasury Department", and further states that

the "Bureau of Internal Revenue" was an "informal" name

which was "formally re-designated the IRS, 1953."

1. 26 U.S.C. § 7803 authorizes the employment of

persons, who, Congressman Danner states, "comprise the IRS". Such authorization of employment of persons

still does not constitute the statutory establishment of an agency known as

"Internal Revenue Service". In fact, in 26 U.S.C.§

7802(b)(1), entitled "Establishment of office" is referenced an

"Office of Employee Plans and Exempt Organizations", which is

"within the Internal Revenue Service" -- but the establishment of the

"Internal Revenue Service" itself is never cited. The term

"Internal Revenue Service" just sort of pops out of nowhere, as if it

already existed as an entity. If the statute authorizing the

"Establishment of [an] Office of Employee Plans and Exempt

Organizations" can be found -- "within the Internal Revenue

Service" -- then why cannot someone produce the statute, which created the

establishment of the "Internal Revenue Service" itself? Since your Appointment Affidavit (see #3

below) states that you’re the "Commissioner of IRS" -- i.e., Commissioner of Internal Revenue

Service -- one would naturally believe that you are the primary person who

should be able to lead us to this (so-far) elusive statute. Which "IRS" are you the

Commissioner of?

2. § 7803 and Congressman Danner’s letter both

reference the "internal revenue laws.”

But 48 U.S.C. § 1402 states that the "internal revenue laws"

generally found at (or "as") 2 U.S.C.§ 1 et seq., the Internal Revenue Code, are

relevant to the enforcement of Title III of the National Prohibition Act. If it is these same laws that "IRS"

employees are administering, then I don’t see how those laws are relevant to

me, or, if some of them are -- which ones?

3. Both Treasury Order 150-25 (March 8, 1951),

and Internal Revenue Manual Delegation Order No. 4 clearly reveal the existence

of two Commissioners, each with different delegated authority: a Commissioner of Internal Revenue (as cited

in 26 U.S.C. § 7802, and the 1862 Act) and a Commissioner of Internal Revenue

Service. As I stated above, your

Appointment Affidavit clearly shows that you are the "Commissioner of

IRS" -- i.e., the

"Commissioner of Internal Revenue Service.” It is apparent that these two Commissioners

each have different delegated authority, and that the Commissioner of Internal

Revenue, referred to in IRM 1111.2 and in Congressman Danner’s letter, is not

you, nor your office.

Since, I have reached the conclusion

that an agency known as "Internal Revenue Service" has never been

actually created by Congress, I am hereby requesting that you provide to me the

citation of any statute(s) which really did create the/an "Internal

Revenue Service" (other than the "Internal Revenue Service"

referenced in the Federal Register, which is admittedly only a term replacing

another term, and clearly not an agency) and the "Internal Revenue

Service" which is the name replacing the "Bureau of Internal

Revenue", which bureau appears to have been established in the Philippines

in 1904. If the Bureau of Internal

Revenue from the Philippine Commission of 1904 is the same Bureau of Internal

Revenue which was renamed "Internal Revenue Service" in 1953, then

please provide documents clarifying that fact, and please then explain to us

how a Philippine Bureau of Internal Revenue, alias (renamed) "Internal

Revenue Service", is relevant to a Citizen of the United States of

America.

Since your Web page makes the public

pronouncement that the "tax collection agency" of which you are the

head was "created" in 1862, certainly you, as the head of this

alleged agency, which posted this public pronouncement to your Web page, should

be easily and immediately able to produce the documents, which support your

pronouncement. If you cannot, then you

are disseminating incorrect and misleading information through your Web site. Relevant to my needing documentation to

support pronouncements by the government:

please be advised of the following:

"No constitutional right exists under the Ninth Amendment, or to

any other provision of the Constitution of the United States, ‘‘to trust the

Federal Government and to rely on the integrity of its pronouncements.’’" MAPCO, Inc. v Carter (1978, Em Ct App) 573 F2d 1268, cert den 437 us 904, 57 L Ed 2d

1134, 98 S Ct 3090. Please do not

respond to the above request by citing 26 U.S.C. § 7802 or 26 U.S.C. § 7803. As

I have stated, 26 U.S.C. § 7802 merely authorizes the establishment of the

Commissioner of Internal Revenue (not the Commissioner of IRS) and does not

reveal the establishment of either a "Bureau of Internal Revenue" or

of an agency known as "Internal Revenue Service.” 26 U.S.C. § 7803 authorizes the employment of

"such persons as the Secretary [of the Treasury] deems proper for the

administration and enforcement of the internal revenue laws" but certainly

does not reveal the establishment of an agency called "Internal Revenue

Service.” 26 U.S.C. § 7802 and § 7803

also raise these questions:

1. Is the "Secretary"

referred to in 26 U.S.C. § 7803 the Secretary of the Treasury of the United

States of America, or the Secretary of the Treasury of the Department of the

Treasury of Puerto Rico, and what statutes or other documents clarify this?

2. Are the

"internal revenue laws" referred to in 26 U.S.C. § 7803 the same

"internal revenue laws" which are relevant to the enforcement of

Title III of the National Prohibition Act?

If they are not, then what statutes or other documents clarify

this? I am also requesting that you

inform me where in the Department of the Treasury (of the United States, not of

Puerto Rico) "Internal Revenue Service" is located and listed as an

agency, and provide me with the statutes to verify its establishment and

location therein.

Finally, I am also asking you to

provide me with a clear and statutorily supported statement which clarifies

exactly which internal revenue laws "generally located" in the entire

Internal Revenue Code are relevant to anything other than and/or in addition to

the enforcement of Title III of the National Prohibition Act (which was moved

to the Virgin Islands and Puerto Rico) and an explanation of why all seized

property is handed over to the assistant regional commissioner (alcohol,

tobacco and firearms). I also need to

know why the Transaction Code 150, designating Virgin Islands [exclusive

federal jurisdiction], is posted to the IMF whenever a Form 1040 is filed, or a

SFR is filed by IRS.

Since this letter contains questions

of profound personal and national importance, I am requesting that you provide

me with the requested answers as soon as possible, or within the amount of time

allotted for an information letter pursuant to the instant Revenue Rulings. Failing a response within that time period, I

shall conclude that you can find no such statute(s) responsive to my request,

nor responses to my other questions, and I shall act accordingly.

Thank you for your attention to this

matter.

Sincerely,

Requester

Special

thanks to Gerald Brown author of In

Their Own Words and Cooperative

Federalism for the preceding research.